Premium updates for 2025-26

Changes to workers compensation premium rates for 2025-26.

The average rate of workers compensation premiums in New South Wales will increase by 8% in the 2025-26 financial year.

The increase is in line with a statutory direction made last year by Workplace Health and Safety Minister Sophie Cotsis, capping the average rate of increase at 8% per annum over three consecutive years (2023-24 to 2025-26).

Individual employers are advised that their own premium may vary from the 8% average, with a final rate calculated according to their specific industry, claims history, safety performance, and other risk factors.

Support is available to employers seeking to lower their premium, with discounts of up to 5% for upfront payment in full, and rewards for safer employers.

Further details on the premium rates for 2025-26 are available in the Frequently Asked Questions below, and there is further information for both small and large employers on how your premium is calculated.

Minimum premium

The minimum premium payable for a policy will increase from $225 to $240 for policy renewal year 2025-26.

Loss Prevention and Recovery (LPR)

icare has enhanced the LPR model to better reward employers who demonstrate strong health and safety outcomes. These updates are part of our ongoing commitment to making the scheme fairer, more transparent, and more aligned to performance.

A refreshed minimum premium formula that more accurately reflects risk means employers with excellent safety performance and effective injury recovery practices may see lower minimum premiums, ensuring that premium contributions are better aligned with individual performance.

Visit the LPR Premium Model page for more information.

Safe Employer Reward (SER)

The Safe Employer Reward (SER) is a performance-based incentive offered to employers who demonstrate a strong safety record and good claims performance. It can lead to a premium reduction at policy renewal.

SER eligibility will be expanded to include the requirement of all employers to submit their actual wages declaration form within four months of the policy period expiring. This means the first policies impacted are those renewing on or after 30 June 2026, providing employers time to prepare, understand their obligations and declare wages upon the completion of each policy period.

Visit the Declaring wages page for further information and support.

- How much are workers compensation insurance premium rates going to rise for NSW employers for the 2025-26 financial year?

- Why are premium rates increasing?

- What is the Safe Employer Reward (SER), and what will change?

- What are Workers Compensation Industry Classification rates (WICs)?

- Why has icare increased the minimum premium charge?

- What can employers do to help reduce their premiums in future years?

- What options do employers have if they cannot pay their premium in full?

- What are Wage Declarations and why are they important?

- What happens if I don't declare my wages?

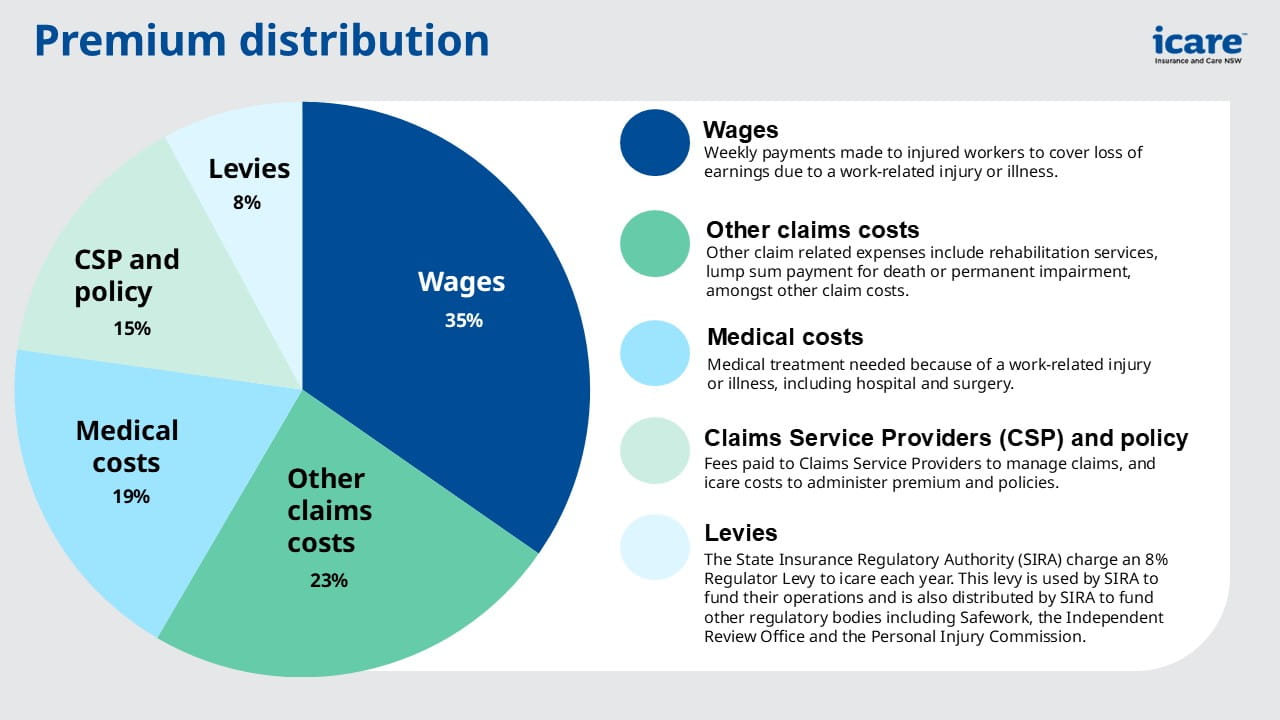

- How is my premium distributed?

- Will premium capping still apply to premiums in 2025-26?

- How do I know if my business is eligible for the Loss Prevention and Recovery (LPR) or LPR Plus products?

- Where do I go if I have questions?

{kind=link}