What is grouping and how does it work?

Continuing our deep dive into some of the more complex aspects of pricing, this week we look closely at employer grouping and what this means for an employer’s premium.

Updated 27 October 2023

What is grouping?

Grouping is where related businesses are required to group their workers compensation insurance. Grouping of policies affects how premiums are determined for each member of the group.Businesses are related if they have shared ownership, control or shareholding of greater than 50 per cent, or if they share employees between businesses.

Employer grouping is regulated by the State Insurance Regulatory Authority (SIRA) within the MPPGs.

Who does grouping apply to?

Employers who are related to businesses with NSW workers insurance policies and combined annual wages of over $750,000 are required to register as a group for workers insurance purposes. Grouping does not apply to employers who are:- self-insured insured or with specialised insurers

- government departments

- related to other employers where their combined annual wages payable to workers does not exceed $750,000

- insured where the policy relates only to private household domestic workers.

When is grouping applied?

Related businesses are required to register as a group when they take out a new policy, or within 14 days of becoming aware that they are part of a group of related businesses. Employers can register for grouping by completing an online grouping registration form. Their policy will then become known as a ‘grouped policy’ and they will be grouped for premium calculation purposes from the group renewal date.

How do grouped policies differ from standalone policies?

Grouped policies differ as their employer size category is assessed at the group level and this impacts how their premiums are calculated.

With grouped policies, all members of the group will have the same renewal date and premiums for each group member will be calculated at the same time.

For conventional policies, where a group is experience-rated, the claims of individual group members do not impact the premium of other group members, unless a group member with claims ceases trading and its policy is cancelled. The claims history of the cancelled policy may be applied to other group members under Group Apportionment.

How does grouping affect an employer’s premium?

The one and only change that is important to understand is that each member of the group will be allocated to the same employer size category used for experience rating.

This is determined by adding the Average Performance Premium (APP) of all employers in the group. It is the group’s total APP that will determine the employer size category for each employer within the group. As shown below there are eight categories.

Employer size categories by APP ranges

- Category 1: >$30,000 to $50,000

- Category 2: >$50,000 to $100,000

- Category 3: >$100,000 to $200,000

- Category 4: >$200,000 to $300,000

- Category 5: >$300,000 to $500,000

- Category 6: >$500,000 to $1,000,000

- Category 7: >$1,000,000 to $2,000,000

- Category 8: >$2,000,000

Once a group's employer size has been determined and allocated to each policy, the premium formula is the same as for any other experience-rated policy.

If an employer in a group has low claims costs and their claims performance is better than the NSW workers insurance scheme performance, using the group's employer size category in the premium calculation is likely to produce a lower premium than if the employer’s policy was not grouped. In this way, grouping can be beneficial to employers, however the opposite can be said for employers who have demonstrated to be a higher risk.

What have we learnt about grouping?

icare is supportive of the principles of grouping and its inclusion within the MPPG. That said, when the Joint Premium and Prudential Oversight Committee (JPPOC) reviewed the premium model, grouping was shown to create large premium swings in either direction for smaller employers within large groups.

icare has submitted alternative options to the JPPOC for consideration in an attempt to provide greater premium stability for these employers.

Grouping methodology

Standalone policies

- no shared ownership or control of greater than 50%

- no employees that work between companies

- claims will impact your policy if you're experience-rated.

(Figure 1) Standalone policies example: Companies A, B and C are standalone businesses that don't meet the grouping registration requirements. The premium for each business is calculated independently.

Grouped policies

May be related through:

- ownership or control of greater than 50% in two or more entities (for example through common directors, ultimate holding company, shareholding, beneficiary of a trust, tracing of interests in a corporation)

- shared employees.

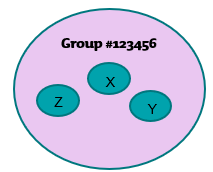

(Figure 2) Grouped policies example: Companies X, Y and X meet the grouping registration requirements. The premium for each business is calculated at the same time.

- each company has the same group number

- separate policy for each member of the group, but common renewal date

- employer size category will be determined by the group's APP

- claims will impact each policy individually if the group is experience-rated.

What's next?

We return to the premium model and look at some of the ways we are looking to enhance the model going forward.

In the meantime, if you’d like to learn more about workers insurance premiums, please visit our How to lower your workers insurance premium page.